Narratives, Capital, and the Climate Transition: 20 Latin Investors on What’s Ahead

How is climate investment evolving in today’s complex landscape? We spoke with those who assess ideas, back teams, and put capital at risk every day to drive real solutions.

We’re living through an era of profound change. China is challenging U.S. hegemony, and global geopolitics is realigning, with armed conflicts bringing issues like energy and food sovereignty to the forefront. Technology is advancing at breakneck speed, making it hard to keep up with AI, robotics, biotechnology, and other disruptions poised to transform our lives. Demographics in our countries are changing, and most Western nations could face steep declines in birth rates and aging populations by the second half of this century. Consensus that once seemed stable has fractured, and climate action has felt the impact—especially with the U.S. pivoting from a federal package to drive the energy transition toward supporting fossil fuels. Meanwhile, pressure on planetary boundaries is real, and issues like water security, climate adaptation, and energy security are more firmly embedded in corporate agendas.

How is climate investment adjusting to this context?

In this edition, we spoke with those who evaluate ideas, support teams, and risk capital in solutions every day in Latin America.

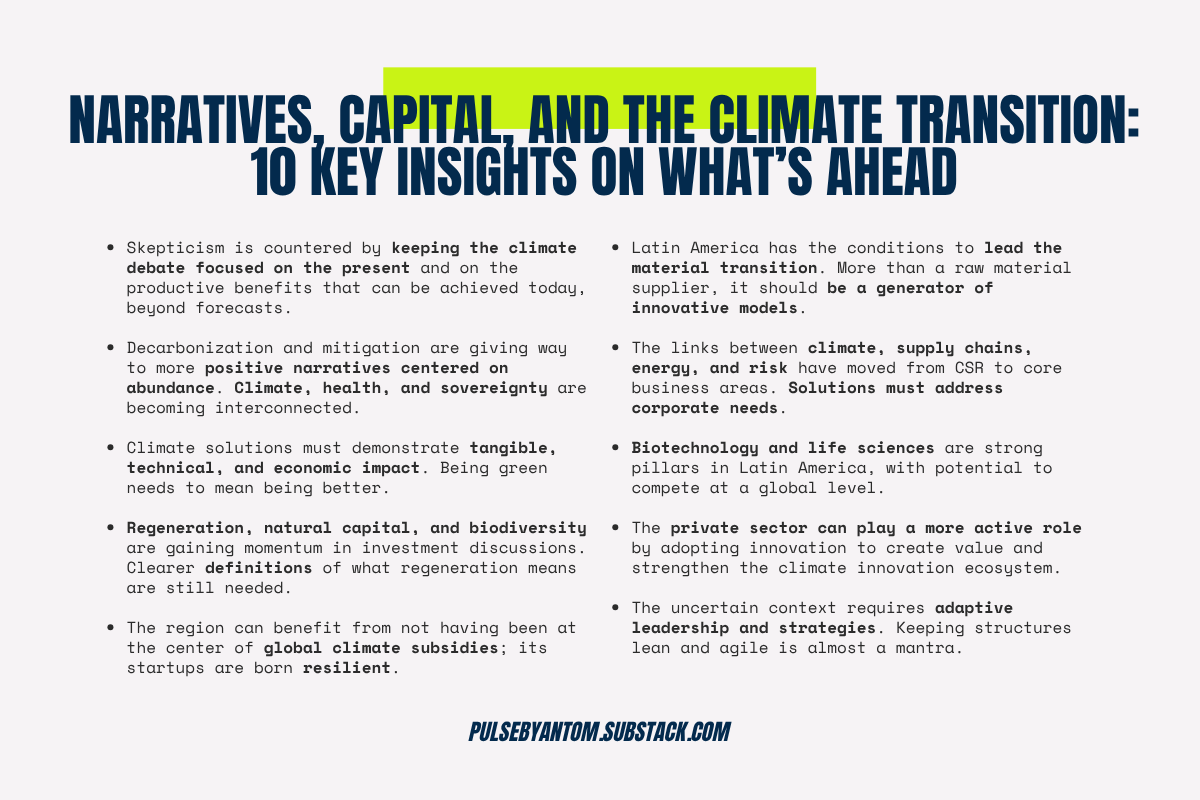

There’s clear agreement: the urgency of the climate crisis isn’t in question, but today’s solutions need to deliver tangible, technical, and economic impact. It’s not enough to be green—you have to be better.

Opportunities are also emerging: the fact that Latin America hasn’t been at the center of global climate subsidies can, paradoxically, work in its favor. Because here, startups are born knowing they have to operate without a safety net.

What’s clear is that the region can and should find its place on this new map not just as a provider of raw materials, but as a generator of models. As a place of invention.

In this email edition, we’re sharing an excerpt of the opinions we gathered. On Substack, we’re publishing the full interviews, along with the agenda of events and open calls. As always, we invite you to join the conversation with a comment or by replying to the email.

A huge thank you to the investors who shared their views! Let’s keep building a regenerative economy for Latam 💪🏼

Matías Peire. Founder and CEO, GRIDX (Argentina)

The way to counter this decline in visibility and interest in impact or climate action narratives is to focus the climate discussion less on the future and more on the present. There’s an opportunity in really understanding these challenges and making production more sustainable for its own productive benefits. That’s always been true for us, but it’s even more pronounced now. And in the end, it will bring about the real solutions the world needs—ones that will naturally and genuinely displace unsustainable practices.

It always seemed like the problem was distant in Latin America because we’re not major carbon dioxide emitters. But if we use the planetary boundaries framework, the problem is very close. Land use and food production contribute far more to breaching those boundaries than greenhouse gas emissions do. And we’re major food producers: we depend on nature to maintain that advantage and our place in the world. If we don’t adapt, Latin America’s productive system will suffer greatly. But I see an opportunity for that adaptation to come from within the region itself.

Laura Ortiz Montemayor. Chief Purpose Officer, SVX México, and GP, Regenera Ventures Fund (Mexico)

I’d said that 2024 would finally be the year when natural capital would break into the financial mainstream, and I think it happened. It was the first time the biodiversity COP had more momentum than the climate change COP. That has major implications for the natural capital sector.

One of the challenges is to stop seeing Latin America as the world’s commodity bank and start becoming the world’s biodiversity laboratory. We need to overcome these extractivist, neo-colonial ideas that seek to monetize biodiversity for the benefit of the global North at the expense of the global South.

Another huge challenge is the sacrifice zones: the energy transition relies on mining in the global South. We have to stand together and support local communities. But that doesn’t overshadow the fact that a regenerative transition across Latin America is a huge opportunity; we need to keep building the conditions for life to thrive.

Timothy Rann. Managing Partner, Mercy Corps Ventures (Ecuador)

In the US the corporate world is trying to figure out where the lines are drawn as it relates to diversity, equity inclusion, to ESG, to climate, because the new administration has shifted its rhetoric and policies. But most of the companies are still either overtly or silently continuing to integrate climate risk analytics into what they do. How climate relates to supply chain, energy usage, energy sources, risk–these are just business principles now, and companies are still committing resources to it. Europe is taking another stand. They’re saying, if you want to sell agricultural or nature-based commodities into the EU, those products need to meet sustainability standards. That’s a shift—from a voluntary regime to a mandated one. Offering tools and resources for compliance opens up new market opportunities for emerging markets.

Capital is indeed shifting—fast. Insurers are pulling out of parts of California and Florida because they’re simply not insurable anymore. They’re not waiting for permission. But if the transition is purely market-driven, it’ll not only be slower, it’ll be exclusionary.

Despite that, there’s a lot of potential for Latin America not just to participate in the transition, but to lead parts of it. In the U.S. or Europe, you’ve got huge entrenched industries with massive interests in maintaining the status quo. That exists in Latin America too, but there's more openness to rethinking systems.

Juan Pablo Garavaglia. Founder and CEO, ARCHE (Argentina)

Climate issues need to have commercial viability; they have to be profitable first and then climate-focused—that’s the rule now.

Latin America remains an immature ecosystem, with few players focused on climate impact and little available capital. In climate tech, we see two or three very good startups per year; the rest still have a long way to go. Biotech and AI continue to be strong pillars in the region, and some capital shows up because there’s global interest in them, plus the quality of startups in those areas is very high—world-class.

We haven’t changed our thesis, but we have changed how we assess the growth potential of startups. Today it’s harder for local startups to keep expanding beyond the region.

We’re preparing a specific project outside of ARCHE to attract European capital to regenerative projects in Latin America. There’s a lot of talk about regeneration, but when you look for projects with real potential to scale, there are few. We see interesting opportunities in Argentina, Colombia, Mexico, and Costa Rica. There’s a lot of work to be done, even though the potential is there.

Sunna Ventures Team (Mexico/United States)

The shift in context is partly due to the lack of concrete results from some of the technologies promoted over the past decade, and a growing demand for more pragmatic, profitable, and scalable solutions.

The narrative is evolving: from a philanthropic view of sustainability toward one centered on efficiency, impact, and economic return. Concepts like “energy security” have gained prominence, driving the energy transition not just for environmental reasons but also for strategic and economic necessity. This represents an opportunity for Latin America: to be a critical part of the global solution from a competitive and structurally necessary angle.

At Sunna, we’re adjusting our thesis to take a step back in the value chain. Instead of focusing exclusively on end-consumer solutions, we’re looking for enabling technologies in strategic sectors for the energy transition: critical minerals, industrial automation and robotics, energy resilience, and climate adaptation solutions. These areas are fundamental for unlocking bottlenecks in the transition.

One of the main challenges in the region is developing climate business models that don’t rely on subsidies or regulatory policies but stand on their intrinsic value in operational efficiency, cost reduction, and scalability.

Galit Flasterstein. Managing partner, Danta Fund (Costa Rica)

In agtech, climate solutions can be viewed from two perspectives. Farmers are interested in sustainability, but—first and foremost—they care about the effectiveness of their business. In both the United States and Latin America, farmers are constantly approached to adopt sustainable solutions, but if those don’t lead to cost savings and higher production, they’re not willing to adopt them.

On the other hand, there are large corporations that have a mandate to become more sustainable but whose client is the farmer. The solutions that startups offer need to deliver both a commercial benefit and sustainability.

Most of the applications we receive at Danta Fund already consider sustainability. However, our thesis and startup selection first analyze commercial success, and then environmental benefit. Since we invest at such early stages, the environmental benefit can’t yet be measured—but the commercial one can be validated with field trials.

Andrés Baehr. Managing partner, Savia Ventures (Mexico)

[The shift in context] means we have to forget about the “green premium” and look for value propositions that focus on cost savings or increased profits. Startups in the region are already adapted to this reality or will have to incorporate it. That’s actually an advantage for Latin America, where startups are used to operating without subsidies.

Companies need solutions to lower energy costs, reduce water consumption, and more. Whether it’s “climate action” or not is irrelevant.

We’re at a moment of opportunity, especially in climate deep tech. The need for these solutions will only grow. Corporations are under increasing financial and operational pressure to mitigate climate impacts in their value chains. I see the scenario we want to create: Latin America as a huge incubator of climate solutions tackling problems at a global scale. Unlocked potential and big money for those who saw this opportunity.

Waldo Soto Bruna. Co-founder and director, 2811, and co-founder, Reciprocal (Chile)

If we assume we live in uncertainty, then it shouldn’t surprise us. The key is how we respond: the present demands adaptive strategies and leaderships. You can’t depend on a single client or product; you need to look for mixed revenue models, avoid “one-shot” sales, and diversify funding sources. Not everything has to come from the market: in Bolivia, the UK is making significant investments in the lithium battery sector, opening opportunities for many local companies.

It seems obvious, but it’s worth repeating: we have to solve real problems. Now more than ever, solutions need to have a scientific basis, measurable impact, and address a need for both the market and society.

It’s also a time to keep companies lean. With AI, global talent, and more flexible structures, it doesn’t make sense to keep oversized organizations. Staying agile is almost a mantra. One more thing: dedicating time and energy to legitimacy.

Tomás Rauch. Investor, Tech Energy Ventures (Argentina)

The shift in context reflects a deep geopolitical reconfiguration, where the climate push driven by Western political agendas is giving way to narratives centered on energy sovereignty, industrial protection, and public spending efficiency. Even so, global investments in the energy transition continue to grow; the structural opportunity remains. The focus is shifting away from relying on subsidies or regulatory mandates toward business models capable of delivering cleaner, cheaper products and/or energy through technological merit. Regions like ours (rich in resources) can leverage that competitive advantage to scale sectors such as solar and batteries, critical minerals, advanced geothermal, or sustainable fuels.

The energy sector is going through a historic moment. It’s projected that electricity demand in the US will double over the next 20 years, with nearly 80% of it expected to be met with renewable energy. The growth in global electricity demand—driven by data centers and the relocation of industrial capacity—is creating opportunities for reliable, clean generation technologies. Meanwhile, critical decarbonization challenges in hard-to-abate industries like steel and cement remain.

The main challenge for the region is adapting to a more fragmented world with greater trade barriers and technological dependencies, especially in strategic sectors like electric mobility and storage. We see a scenario with high volatility but also historic opportunities. In a world that is no longer just pursuing decarbonization, but also energy abundance and industrial competitiveness, Latin America can play a key role.

Catalina Taricco Zañartu. COO and CMO, Impacta VC, and President, Chilean Venture Capital Association (Chile)

In Latin America, where we’re already experiencing the consequences of climate change, this kind of skepticism is a risk because it delays the allocation of resources, can slow sustainable innovation, and even discourage urgent public policies. But there’s room for hope. This same context has pushed many people and organizations to double down and act more decisively. From our role as an impact investment fund, we’re committed to supporting concrete climate solutions that are not only sustainable but regenerative.

We see enormous opportunity in entrepreneurs creating regenerative, resilient, and scalable proposals. In contexts of denial or backsliding, it makes even more sense to mobilize purpose-driven capital.

Latin America faces major gaps in infrastructure for innovation and in technological development. But that’s also why there’s so much to build. Investing in regenerative solutions is a real business opportunity. It’s an attractive investment thesis, with competitive returns and growing interest from large funds and institutional investors. Our task as a sector is to keep pushing this transformation with intention, capital, and collaboration so that this opportunity translates into real solutions for the region and the planet.

Carlos Becco. Senior agtech advisor, author of the books “The agri digital revolution” and “From Villains to Heroes” (Argentina)

The scientific evidence supporting the climate crisis is overwhelming, and the need to work on energy efficiency is essential. The more skeptical narratives that have emerged in some global power centers are driven by sectoral interests trying to defend a position of privilege. Unfortunately, they create confusion and may slow the progress of climate tech projects—though they won’t stop them. The sustainability component has become an essential requirement in every investment project we support or invest in.

Every week I get news about new investment funds arriving in the region, where the focus on climate or regenerative solutions is either a priority or at least a highly prominent interest. I also see major players in the agricultural sector choosing to bet on innovation.

Gideon Blaauw. Regional lead, CleanTechHub (Colombia)

This year there were many changes driven by the new positioning of the United States. Institutional stances and business strategies are adjusting their visions toward 2030 or 2050. Narratives are shifting too: for example, now people talk about “green growth” instead of “climate change.” That aligns well with our vision because we’ve never promoted ideas of degrowth or limiting growth. We’re not activists. Our entrepreneurial approach has always been tied to innovation, disruption, and growth.

Our economies are more similar to those in Africa or Southeast Asia than to those in Europe or North America. There’s a lot to learn from the Global South; for example, in how to formalize the circular economy, where many structures remain highly informal.

One question we often get is: Do real investment markets even exist in Latin America? We believe they do—but they only respond to truly solid proposals.

Eugenio Cantuarias. Partner, AceleraLatam (Chile)

The shift in narrative doesn’t mean the problem is losing relevance, but rather that there’s a reordering of priorities and expectations in the face of economic, geopolitical, and technological pressures. Latin America doesn’t define global narratives, but it does bear the externalities of climate change: water stress, food insecurity, soil degradation. This increases local urgency and the need for solutions that don’t depend on global agreements.

The main challenge for the region is the lack of patient capital infrastructure. Many funds still have short horizons and a strong appetite for SaaS-style growth, which doesn’t always fit the validation cycles of a climate tech startup. There’s also real asymmetry in technical knowledge between founders and investors. Many regenerative deep tech solutions require technical networks, not just capital. And there’s a lack of clear, simple, auditable, and scalable ways to measure regenerative impact.

The investment climate doesn’t depend on ideological conviction, but on proving that solving the region’s biggest problem is good business.

Erika Sánchez Herrera. Coordinator of the CATAL1.5°T Initiative, German Technical Cooperation (GIZ) in Mexico

In Latin America, a momentum toward climate action has been created. While it will face challenges, it will not stop. At CATAL1.5°T, we’ve seen firsthand the positive impact of investing in climate and tech entrepreneurship, which is why we’re committed to continuing to strengthen the climate tech ecosystem in the region. The ventures we pick don’t just have climate impact—they also feature innovative business models, social impact, public benefit, and criteria for inclusion, diversity, and gender.

Entrepreneurs face challenges such as access to financing and developing the pipeline and bridging ecosystem gaps. As long as we don’t solve those barriers, growth will remain limited—and so will the consolidation of climate technologies.

Juan Soria. Managing partner, SF500 (Argentina)

What’s being debated now is whether a green solution can justify a premium. If it’s faster, better, and cheaper, then it can scale and compete. From our investment thesis, we continue to back science-based startups, in verticals ranging from human health to the planet. The focus on climate remains a priority, but we have to be more creative and demanding. These solutions need to build real competitive advantages tied to performance, price, and scalability. More is expected of them than a few years ago.

We’re in a moment of greater uncertainty, but in the long term, the consequences of climate change are well documented, visible, and it’s only a matter of time before that reality pushes investment in this category again.

Facundo Garretón. Founder and CEO, Terraflos (Argentina)

The climate debate is maturing. We don’t see denial, but rather a tension between different approaches and short-term economic priorities. At the same time, there’s an acceleration in the search for concrete solutions from the private sector.

For Latin America, this represents a strategic opportunity: we’re a region with high biodiversity, a key role in the bioeconomy, and enormous potential to lead climate solutions based on science, regeneration, and sustainable production. But we need to build our own narrative and technological capacity, not just be suppliers of commodities or carbon offsets. We need to stop merely reacting to global agendas and start building solutions from our bioeconomic identity.

We see three clear opportunities: regenerative bioeconomy (functional foods, science-based cosmetics, supplements produced without planting), decentralized and adaptive technologies (from biotechnology to cellular agriculture and AI applied to health and climate), and new investment frameworks (patient capital, hybrid funds, and investors seeking real, measurable impact with returns).

Christian Daube. Climate Innovation Lead, Latin America and the Caribbean, Climate-KIC (Denmark)

Climate solutions must focus on how to develop the region, or on looking toward similar markets—like Asia and Africa—where the challenges are the same (and unfortunately will keep growing). More investment is needed, especially through blended finance mechanisms that can help scale innovations willing to take on the risk of contributing to sustainability and regeneration.

Companies—big and small—need to work more with innovation to generate real benefits. There are few investors, and that’s not going to change in the short term, so the private sector must take a more active role in implementing innovations and strengthening the climate innovation ecosystem.

Diego Serebrisky. Co-founder and managing partner, Dalus Capital (Mexico)

For Latin America there will probably be less capital available, especially that which used to come from public agencies or U.S. government programs. But on the other hand, it remains a priority for many governments and private actors. We believe that the development of solutions—from both the public and private sectors—will continue. A third of our latest fund is focused on climate innovation startups, and that commitment remains. In fact, we’re actively looking for opportunities.

The biggest challenge remains the availability of financing. But we’re already seeing initiatives for funds with a 100% climate focus, at different stages, both in debt and potentially in equity. We believe that will grow significantly in the coming months and next year. So we continue to see a positive trend. The conversations we’re having, both with large investors and with funds looking to allocate more climate capital, indicate this isn’t going to stop.

Matías Kelly. Founder, Sumatoria, and partner, Beta Impacto VC (Argentina)

The current context can be an opportunity if we manage to frame climate solutions as part of a broader development agenda: job creation, strengthening local communities, productive diversification, financial inclusion. If the climate message becomes something useful and relevant, the room for action grows.

Global tensions make us cautious about the risks of certain “green” financial mechanisms that don’t always benefit local communities or the most vulnerable actors. That’s why we reinforce our focus on patient financing with a strong emphasis on purpose. Many climate solutions require scales and timelines that the traditional financial system isn’t always prepared to support. But we see an opportunity in the growth of an “impact infrastructure” that is starting to consolidate.

We imagine an ecosystem where climate financing is less concentrated in large projects and more focused on thousands of small and medium solutions, distributed across territories, combining innovation, regeneration, and inclusive development.

Ruben Altman. Co-founder and CEO, Antom.la

Some of the criticism to environmental narratives is valid: there’s fatigue around greenwashing and solutions that rely more on external incentives than real value propositions. The current context is helping us filter them out.

We see growing consensus around human health. And in most cases, the health of the planet and the health of people are deeply connected. We see real opportunities in bioproducts, biomaterials, new production methods. Also in digital tools for making better, more agile decisions, and in financial instruments that help solutions scale.

Latin America faces both the challenge and the opportunity of transforming an economy based on food production and adapting to a new climate, technological, and geopolitical reality. We have everything needed to lead this transition—but also the risk of letting others define the path for us. If we can work together intelligently, the region has the potential to offer the world a different vision of development: one that doesn’t just adapt but proposes.

If you’ve made it this far and want more, remember that on Substack we’re publishing the full interviews and the agenda of open calls.

As always, you can leave a comment or reply to this email if you have feedback or want to add something to the conversation.

Thanks again to everyone who contributed to this piece! Until next time!